.png?width=180&height=65&name=Untitled%20design%20(29).png "Untitled design (29)")

As an insurance agent, one of the most important responsibilities you have is to properly protect your clients. This means ensuring that they have the coverage they need to protect themselves and their assets, as well as educating them about potential risks and ways to mitigate them. Day to day it can be easy to forget that this is the ultimate goal as we are all either running or working in a sales organization where the primary objective is to close more business.

Unfortunately, not all agents weigh the responsibility of protecting their clients as seriously as they weigh their monthly and annual sales goals and quotas, and this can lead to disastrous consequences for their clients.

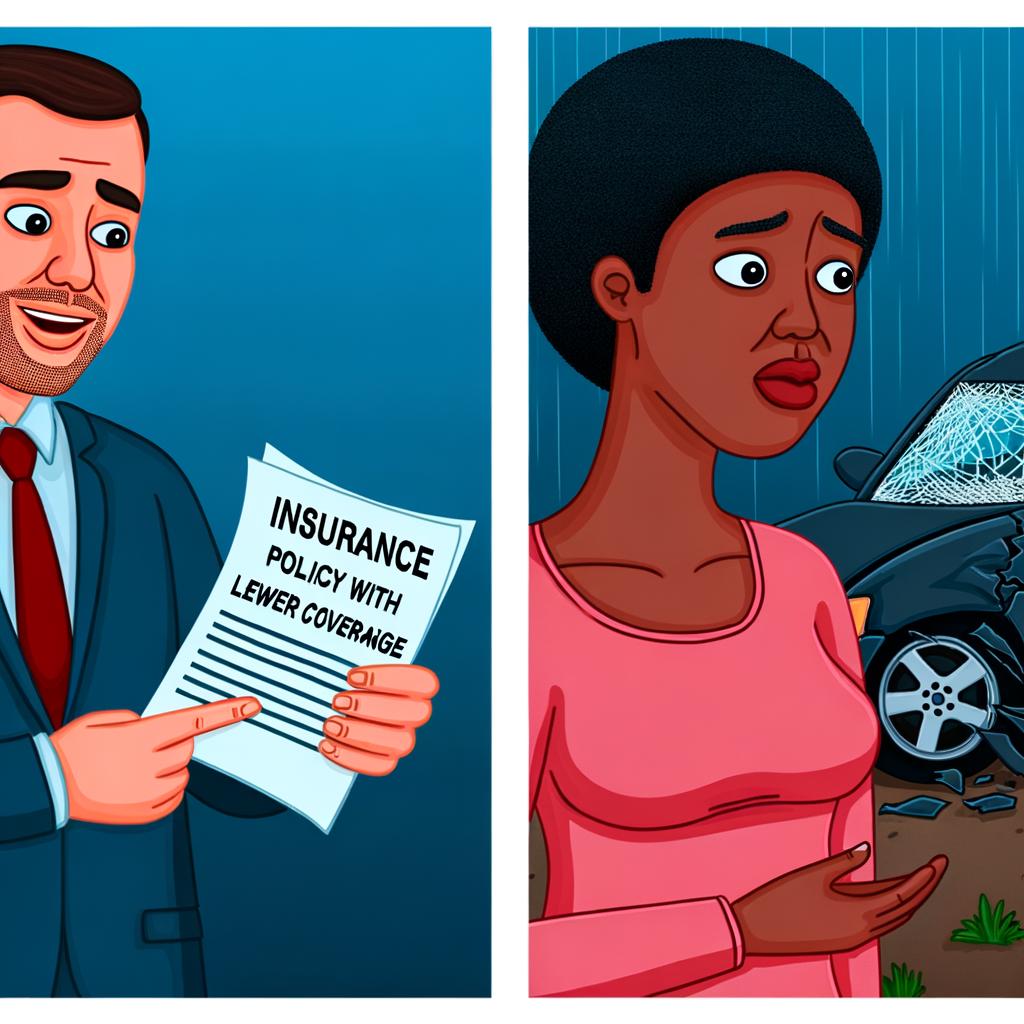

Take the case of Jack, a new insurance agent who was eager to earn some appointments with a number of carriers. John had a prospect named Diane who was looking to save money on her car insurance. Diane had been with her previous insurance company for years and had a policy with high limits that gave her peace of mind.

When Jack quoted her however, Jack was not able to price a similar policy competitively. He thought fast and saw an opportunity to make the sale by offering her a lower-priced policy with lower limits. He didn't tell Diane that he was lowering her coverage, and she assumed that the new policy would offer the same protection as her old one.

A few months later, Diane was in a serious car accident that was her fault. She was sued for damages to the tune of $712,000 and found herself owing a lot of money that would have been covered by her old policy. When she contacted Jack to file a claim, she discovered that her coverage was much lower than she thought, and she would have to pay a significant portion of the damages out of pocket. The claim was only going to cover $50,000 of the accident! Diane was devastated, and she realized that she had been misled by Jack. Furthermore she was beginning to deal with a new reality that she was going to be financially devastated for the forseeable future.

In the end, Diane decided to sue Jack for professional negligence. She argued that Jack had breached his duty to her by not providing her with adequate coverage and by failing to disclose the changes he made to her policy. Jack's E&O insurance was forced to pay out a substantial settlement to Diane, which negatively impacted Jack's finances after his $10,000 deductible AND his standing with some current carriers. On top of that, he found getting appointments with new carriers difficult in the near future as they evaluated the risk of bringing on a sloppy Agent. Additionally, Diane was forced to pay out of pocket for damages that would have been covered by her old policy, causing significant financial strain for her as well.

The story of Jack and Diane is a cautionary tale for insurance agents everywhere. Shifting coverage or declining coverages without telling your prospect is not only immoral and unethical, but it can also have severe financial consequences for all involved. Not only is it a breach of your duty to your clients, but it also violates the trust that they place in you as their agent. As an agent, it's important to remember that your clients rely on you to protect them, and it's your responsibility to do so to the best of your ability.

In addition to the ethical considerations, there are also legal and financial consequences for failing to properly protect your clients. As Jack learned the hard way, agents can be sued for professional negligence if they make mistakes that harm their clients. The notion of “Anything for a sale”

is not wise in an industry that serves and protects its customers. This can be financially devastating for both the agent and their E&O insurance provider, as payouts can be substantial. It's crucial for agents to understand that their actions can have long-lasting financial implications for both themselves and their clients.

Ultimately, the story of Jack and Diane is a reminder of the importance of properly protecting your clients as an insurance agent. It's not enough to simply sell them a policy and collect a commission – you have a duty to ensure that they are adequately protected and that they understand the coverage they have. By doing so, you can help your clients avoid financial ruin and build a reputation as a trusted and reliable agent.